How to Set Up an SMSF for Property Investment (2026 Guide)

Everything you need to know before you commit — trustee structures, registration, bare trusts, and realistic timelines.

General information only. For financial advice on whether an SMSF is right for you, speak with a licensed financial adviser.

If you've been told you can use your superannuation to buy property, you're not wrong — but the path to doing it isn't simple. It involves setting up a Self Managed Super Fund (SMSF), choosing the right trustee structure, registering with ASIC and the ATO, and (if you're borrowing) establishing a separate bare trust. This guide walks you through the entire process so you know what to expect before you commit.

Important

Setting up an SMSF involves regulated financial advice. Evolution Lending Partners is a specialist SMSF lending brokerage. We help you structure and secure the loan once your SMSF is established — we do not provide financial advice on whether an SMSF is right for you. For that, please speak with a licensed financial adviser or your accountant. This page is general information only.

Who this guide is for

- › You have $200,000 or more in superannuation (combined with your partner if applicable)

- › You want to use your super to buy investment property — residential or commercial

- › You're comfortable taking more active control over your retirement savings

- › You want to understand the setup process before you commit any money

Decide if an SMSF is right for you

Before any paperwork, take an honest look at whether an SMSF makes sense for your situation. An SMSF is not free, not passive, and not for everyone. The general guidance from the ATO and industry is that an SMSF starts to make financial sense at around $200,000–$250,000 in combined balance, primarily because annual running costs (accounting, audit, ASIC fees) are fixed regardless of fund size.

You'll also need to consider your current super performance, existing insurance inside your superfund, your risk appetite, your tax position, and the level of involvement you're willing to take on. SMSF trustees have legal obligations — you can't just set it and forget it.

Choose your trustee structure

Every SMSF has trustee(s). You have two options:

Individual trustees

Each member of the fund is also a trustee. It's easier and cheaper to set up (no ASIC fees) but more administrative hassle with ongoing management — every time a member is added, removed, or property is bought or sold, all trustee names must appear on every legal document.

Corporate trustee (recommended for property)

A company is the trustee, and the fund members are directors of that company. More expensive upfront (ASIC company registration plus annual review fees), but far cleaner long-term — especially if you plan to buy property, change members, or grow the fund.

Bottom line: For property-focused SMSFs, most lenders and most accountants strongly prefer corporate trustees. If you're planning to borrow to buy property, plan on using a corporate trustee from day one.

Steps 3–7: Establishing and activating the fund

Establish the fund and trust deed

The legal document that governs how the fund operates. The trust deed must comply with the Superannuation Industry (Supervision) Act 1993 (SIS Act). Specifically for property buyers, you want a deed that explicitly permits limited recourse borrowing arrangements (LRBA) for property purchases.

This is also when you'll appoint the trustees (or set up the corporate trustee company), name the members, and decide the investment strategy framework.

Register the fund with the ATO

Within 60 days of establishment, the SMSF must be registered with the Australian Taxation Office. This is when the fund gets its own Tax File Number (TFN) and Australian Business Number (ABN), and elects to be regulated as a complying super fund. This step is usually handled by whoever is setting up your SMSF.

Open the SMSF bank account

The fund needs its own dedicated bank account, completely separate from any personal accounts. All contributions, rollovers, rental income, expenses, and loan repayments flow through this account. Most major Australian banks offer SMSF-specific accounts (you'll need the ABN and TFN for this step).

Roll over your existing super

You contact your current super fund(s) and request a rollover to the new SMSF. This typically takes 1–4 weeks. If you have multiple existing super accounts (e.g. from past employers), you'll need to request rollovers from each superannuation account separately.

Heads up

Some industry super funds have started making the rollover process more difficult than it needs to be. To avoid delays, check that your details are correct and up to date — spelling mistakes, missing hyphens, middle names, and old addresses all cause delays. Also, if you have insurance attached to your existing super (life, TPD, income protection), check what you're giving up before rolling over. Most trustees usually leave 2–3 years of insurance premiums in cash and keep the old account open to ensure sufficient insurance cover.

Establish the fund's investment strategy

The SIS Act requires every SMSF to have a documented investment strategy. This isn't a suggestion — it's a legal requirement. The strategy must consider risk, return, diversification, liquidity, and the fund's ability to pay benefits when due.

For property-focused SMSFs, the strategy should explicitly address the concentration risk of holding a large single asset (a property) and how the fund will maintain liquidity for ongoing expenses and member benefits. This is usually done during the fund setup, as whoever sets up the fund will provide these templates. They will also be requested by the fund's auditor when annual tax returns are lodged.

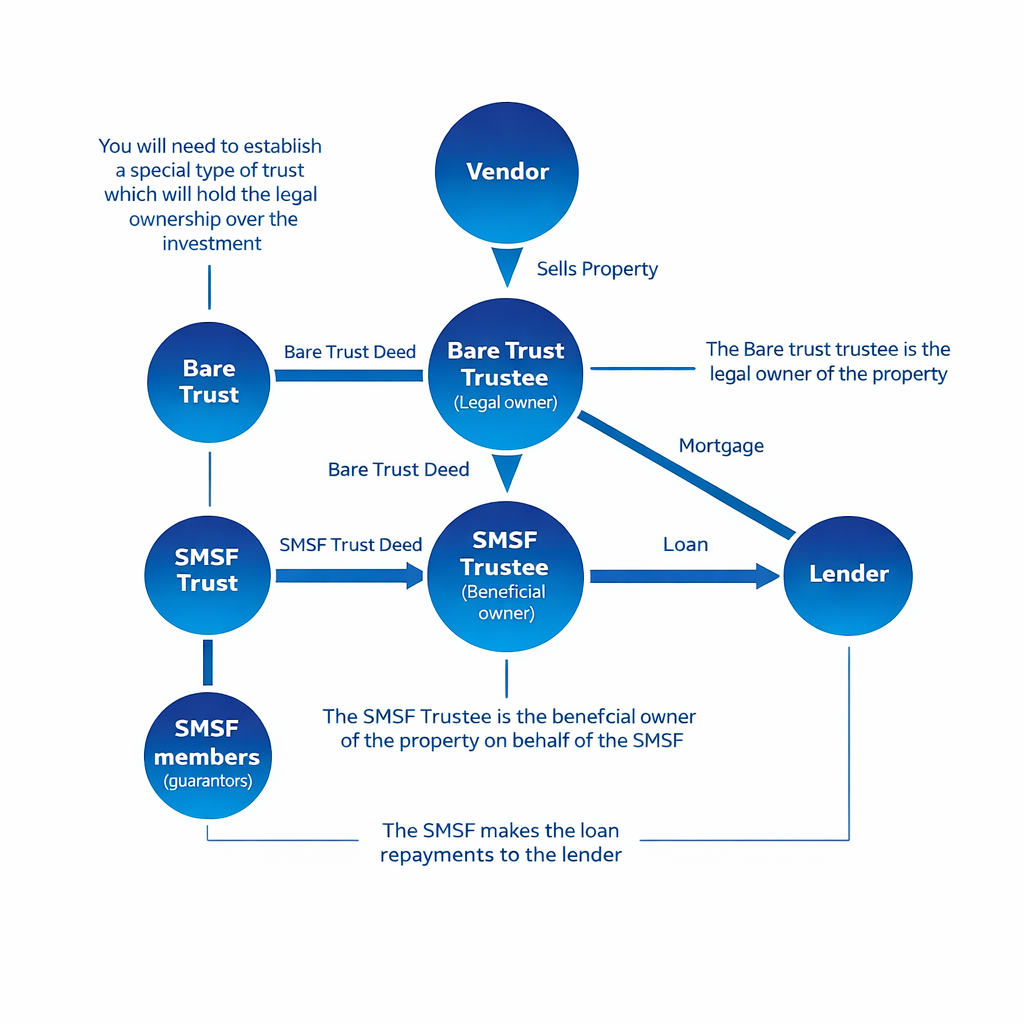

Set up the bare trust for LRBA (property buyers)

If you're going to borrow money to buy property, the loan must be structured as a Limited Recourse Borrowing Arrangement (LRBA). The 'limited recourse' part means if the loan defaults, the lender can only claim the property itself — not other assets of the SMSF.

LRBAs require a separate legal entity — a 'bare trust' (also called a 'custodian trust' or 'holding trust') — to hold the property on behalf of the SMSF until the loan is fully repaid. The bare trust must be established before contracts are exchanged. Getting the order wrong here is one of the most common SMSF property mistakes and can void the entire structure.

Ready to talk about the lending side?

Once your SMSF is established (or you're close), we can assess your borrowing capacity, identify the right lenders for your situation, and get you pre-approved before you start searching for a property.

Book a Free 30-Minute Strategy CallTypical timeline

| Stage | Typical timeframe |

|---|---|

| SMSF establishment and ATO registration | 1–3 weeks |

| Rollover from existing super funds | 1–4 weeks |

| Bare trust setup (if borrowing for property) | ~1 week |

| Loan pre-approval | 48 hours (subject to all documents being available) |

| Property purchase and settlement | 4–6 weeks depending on contract |

Realistic end-to-end timing from 'I want to do this' to 'I own the property': 1–3 months. Faster is possible but rare.

Indicative setup costs

These vary by provider but as a guide:

| Item | Indicative cost |

|---|---|

| SMSF establishment with corporate trustee | $1,500 – $3,500 one-off |

| Bare trust setup for property | $1,500 – $2,500 one-off |

| Annual SMSF accounting and audit | $1,500 – $3,500 per year |

| ASIC corporate trustee annual review fee | ~$329 per year |

Setup and administration costs only. Loan-related costs (application fees, valuation, legal) are separate and depend on the lender and property.

Common mistakes to avoid

Exchanging contracts before the bare trust is set up

This can void the entire arrangement. The bare trust must exist before you sign any property contract.

Using individual trustees when planning to borrow

Most lenders require corporate trustees for SMSF property loans. Setting up individual trustees and then switching later creates unnecessary cost and delay.

Treating the investment strategy as a tick-box exercise

Your auditors look at this closely. A strategy that doesn't address concentration risk or liquidity will attract scrutiny.

Mixing personal and SMSF money

The fund must be completely separate from your personal finances at all times.

Not factoring in liquidity

Your SMSF must always have enough cash to pay expenses, loan repayments, and any pensions due. See how much super you actually need before committing to a purchase.

What happens after setup — the lending conversation

Once your SMSF is established, we can approach lenders. This is where Evolution Lending Partners comes in. We specialise in SMSF property lending and have access to 20+ SMSF lenders.

We help you:

- › Understand which lenders will say yes to your specific situation

- › Structure the loan to maximise serviceability and minimise deposit

- › Navigate residential vs commercial property loan differences

- › Get pre-approved before you start hunting for a property

Next steps

If you've read this far, you're serious about SMSF property investment. Here's what to do next:

- › Once you're committed to the SMSF path, book a free 30-minute strategy call with our lending team. We'll walk you through what lenders will look at, how much you can realistically borrow, and how to structure the purchase.

- › Download our free SMSF Property Investment Guide for a deeper look at lender requirements, deposit needs, and the loan approval process.

Frequently Asked Questions

Do I need at least $200,000 in super to start an SMSF?

There's no legal minimum, but industry guidance and ATO data suggest that under $200,000 the running costs eat into returns too aggressively. For property investment specifically, lenders typically want to see at least $200,000 in the fund post-deposit, so the practical entry point is higher.

Can I live in a property my SMSF buys?

No. SMSF residential property cannot be lived in by you, related parties, or used as a holiday house. It must be rented at arm's length to unrelated tenants. Commercial property has different rules — you can run your business out of an SMSF-owned commercial property as long as the rent is at market rate.

Can I buy property from a family member through my SMSF?

Generally no for residential. The sole exception is business real property (commercial), which can be acquired from a related party at market value. Always confirm with your accountant before going down this path.

How long does the whole setup take?

Realistically 4–10 weeks from first conversation with your accountant to having a fully-functioning SMSF ready to make property offers. If you're rolling over from multiple super funds, the rollover step is often the slowest part.

Can I add my partner to an SMSF I've already set up?

Yes, as long as the trust deed permits multiple members (most modern deeds do). With a corporate trustee structure, your partner becomes an additional director of the trustee company. With individual trustees, you'd need to update every fund document to add them as a trustee.

Ready to talk lending?

If you've worked through Steps 1–7 and you're ready to talk about the lending side — book a free 30-minute strategy call. We'll review your fund structure, talk you through SMSF lender requirements, and give you a realistic view of what you can borrow.

Book a Free SMSF Lending Strategy Call